1. Introduction

The foreign direct investment (FDI) inflows in small island developing states (SIDs) in Africa have substantially increased over the past decades. For example, on average in 2005 it was estimated at $455 million, then in 2017, it increased to $816 million, and in 2018 and 2019 it stood at 719 and 750 million USD respectively. Some studies (Ahmed et al., 2021; Fauzel et al., 2017; Read, 2008; Tillmann, 2013) mentioned that emerging economies encourage foreign capital inflows, mainly as they promote domestic economic development. This is particularly true for small island economies, constrained in terms of resources and their size. The assets possessed by most of the islands are in terms of their natural attractions, unique flora/fauna, and beautiful coastlines (Seetanah, 2011). Such assets have been attracting foreigners to the island states, either for holidays or as real estate investors. Several emerging countries possessing islands (for example, Croatia, and Malaysia, among others) or island states (for example, Mauritius, Malta, and Caribbean islands, among others) have been benefiting from foreign investment in the residential real estate market. These investments mainly represent secondary homes for foreigners, also known as residential tourists. As the residential tourists settle in the island economies, they bring their foreign currency and use it in their daily expenses, which promotes job creation and economic growth on the island.

In the island of Mauritius, FDI inflows have been fluctuating over the past decades, mainly with an increasing tendency, for example in the year 2000 FDI stood at $270 million, it decreased to $110 in 2006 and then increased to $590 million in 2012. In 2018, FDI was at $372 million and it increased to $472 million in 2019 (figures obtained from World Bank). According to UNCTAD’s World Investment Report 2020, a large component of the foreign inflows in Mauritius were directed towards the real estate sector, for example, in 2019, around 81% of the foreign inflows were in the real estate sector. Foreign investment in the Mauritian real estate market has been encouraged through the set up of three main schemes known as the Integrated Resort Scheme (IRS), Real Estate Scheme (RES), and Property Development Scheme (PDS). These schemes allow foreigners and wealthy tourists to purchase luxury residential units (villas) in the domestic market. The first scheme launched in 2001 is the IRS, then the RES was launched in 2007 (with less strict restrictions in terms of the size and value of the investments allowable to foreigners), and subsequently, in 2015 the PDS was set up. The aforementioned schemes allow foreigners to penetrate the Mauritian residential land market and this should entail an increase in land demand.

This study focuses on how foreign real estate investments (FREI) affect residential land prices. Mauritius represents a good context for studying the aforementioned link, and the availability of land prices is explained by the fact that in the residential real estate market most transactions take place in the land market. Apart from determining if foreign land demand affects land prices, the influence of domestic land demand and supply is also assessed. Within the domestic factors prone to affect land prices, latent variables are also considered.

Past studies have used the equilibrium land pricing model to explain the formation of land prices. It was established that changes in demand and supply affect land prices (for example, Gholipour, 2013; Muth, 1971; Rose & La Croix, 1989; Witte, 1975). An increase in land demand should normally culminate in an increase in land prices. Most studies have included fundamental factors (consisting mainly of macroeconomic and demographic factors) as the main determinants of residential real estate prices (Abraham & Hendershott, 1994; Belke & Keil, 2018; Davis & Heathcote, 2007; Geng, 2018; Gottlieb, 1965; Malpezzi, 1999; Mankiw & Weil, 1989; Manning, 1988; Nakamura & Saita, 2007; Poterba, 1991; Tsatsaronis & Zhu, 2004; Witte, 1975). Some studies have used latent variables as explanatory variables for land prices, for example, land regulations, tax relief on mortgage interest payments, or the preferences of land buyers, among others (Algieri, 2013; Fadiga & Wang, 2009; Hannonen, 2005; Huang, 2019). A few studies have probed upon the link between foreign capital inflows and real estate prices, using different measures for capital inflows and mainly focusing on how these have been affecting housing prices (Ahmed et al., 2021; Brooks et al., 2017; Gholipour, 2013; Mihaljek, 2005; Sa, 2016 and Tillmann, 2013, among others). It is noteworthy that a larger literature exists on the influence of domestic factors on real estate prices as compared to foreign factors.

This study attempts to supplement the literature by bringing additional evidence on the determinants of land prices, particularly concerning foreign land demand. It is aimed at establishing whether foreign residential demand has had an impact on residential land prices in Mauritius. It is highlighted that most past studies on the link between foreign real estate investment and real estate prices have essentially focused on housing prices. Over the past decades, residential land prices in Mauritius have undergone significant price increases, this study will help in discerning if these increases are attributed to foreign land demand or other factors. With a better knowledge of the influence of FREI on land prices, the Mauritian government would be able to closely monitor how foreign land demand is affecting domestic land prices and put in place appropriate measures, with the aim of not outpricing local land buyers.

A relatively more accurate measure of foreign investment in the residential real estate market is used in the present study, as compared to past measures applied (for instance Chow & Xie, 2016; Mihaljek, 2005; Tillmann, 2013). The aforementioned studies used more general measure/s of foreign inflows, whilst this study focuses on FDI in the residential real estate market. A structural time series model (STM) is used to find if foreign real estate investment (FREI) has been affecting land prices and also to establish if other factors such as fundamentals or latent variables are explaining land prices. STM enables a more comprehensive assessment of the factors determining land prices, given that the unobserved components found in the model probe upon the link between latent variables and land prices.

The rest of this work is organized as follows: section 2 reviews both the theoretical underpinnings and the related literature, section 3 discusses the methodology, section 4 discusses the findings and section 5 concludes.

2. Related Literature

Theoretical review

Recent studies on land prices consider the equilibrium land-pricing model according to which residential land prices are set through the interaction between land demand and land supply (Geng, 2018; Ho & Ganesan, 1998; Jiang et al., 2013; Manning, 1988; Muth, 1971; Quigley, 1999; Reichert, 1990 and Witte, 1975, among others). The factors affecting land demand and supply can be categorized into three essential groups, namely domestic, foreign, or latent variables.

The factor considered as bearing the most significant influence on land demand is land prices. According to Mankiw & Weil (1989) and Liu et al. (2016), there is an inverse link between land demand and prices. Apart from this main factor, other potential factors have been identified in past research as affecting the demand for housing/land (Algieri, 2013; Asal, 2018; Davis & Heathcote, 2007; Quigley, 1999; Reichert, 1990). These can further be classified as affordability measures such as the level of income, interest rate, or mortgage rates and demographic factors such as population size, the level of employment, and other latent variables (for example tax relief on mortgage interest rates, property taxes, regulations facilitating the purchase of property or ease of access to mortgage loans and speculative land buying among others). Rose & Lacroix (1989) highlighted that apart from domestic factors, foreigners could also be affecting land demand and hence land prices.

Land price also represents a determining factor for land supply. Ooi & Teck Lee (2004) considered that when land supply regulations are strict and land supply is limited then land prices would tend to increase. From past research, common factors used for defining the supply of land are the number of residential construction projects approved (commonly measured using residential building permits) and construction costs (Asal, 2018). Some latent variables such as constraints in the building sector, regulations on land use, or zoning regulations could also be affecting land supply (Glaeser et al., 2005; Kok et al., 2014).

Gholipour (2013) considered three channels through which FREI can affect real estate value. Firstly, as foreigners purchased more real estate, this led to an increase in land demand. The specificity of the land market is in terms of the inelasticity in land supply mainly in the short term, which would entail an increase in land prices. Ahmed et al. (2021) also posited that an increasing real estate demand from foreigners should be occasioning a rise in domestic real estate prices.

The other two channels represent indirect ways through which foreign capital inflows could affect real estate prices. For instance, the second channel is termed a liquidity channel, with foreign investments increasing the domestic money supply as a consequence of which there is an increase in the demand for assets (including real estate demand) and their corresponding prices (see Lu & Dong, 2016). The last channel generating a link between real estate prices and foreign investments is economic growth (normally measured by using the gross domestic product/GDP). Emerging economies are normally perceived as encouraging foreign investments as this promotes their economic development and this consequently leads to an increase in the demand for assets (real estate) and their prices (see Chan, 2007; Gholipour et al., 2014).

Empirical review

Past studies on the link between real estate prices and foreign capital inflows have used different measures for capital inflows and the studies have been undertaken in different contexts. One of the first studies to include foreign investment in land as a determinant of land price and more specifically as a demand side factor within an equilibrium pricing model was Rose & Lacroix (1989). The measure used for foreign investments is proxied by the percentage of families speaking foreign languages, given that no complete record for foreign real estate investments was available. The authors studied Honolulu and 39 other urban regions in the US and it was observed that land prices tend to be higher in Honolulu as compared to the other urban regions in the US in 1980. The other explanatory variables included in the study were population, population growth, amenities, and income. Supply-side factors such as restricted land availability and zoning also contributed to land price increases. Foreigners were purchasing property in Honolulu as a secondary home. The variable foreign buyers had a significant and positive effect on land prices in Honolulu and it led to a marginal increase of 34% in land prices.

Studies on the link between foreign investment and real estate prices have essentially been conducted within developing countries’ contexts and/or emerging markets. Studying the Croatian real estate market, Mihaljek (2005) noted that most foreign real estate purchases occurred in coastal regions or on islands. Using a conceptual research approach, the author observed that real estate and land values in the regions attracting FREI have been increasing and in certain cases, the rise in prices took place before the conclusion of the transactions. Such price increases were justified through the expectations channel, where actual real estate prices increased in anticipation of the rising future demand made by foreigners. Mihaljek (2005) also suggested that FREI could lead to affordability issues in the domestic real estate market. Although the author acknowledged that part of the land price increase was due to foreign demand, it was also pointed out that other domestic factors were important in explaining the land prices.

Gholipour (2013) studied the influence of FREI on housing prices in 21 emerging countries over the period 2000 – 2008 by using a panel VAR approach and concluded that FREI had a significant positive influence on housing prices, albeit relatively small in magnitude. Using a similar approach, Tillmann (2013) found that foreign capital inflows had a significant positive influence on property prices in some Asian countries (for example, Korea, Hong Kong, Malaysia, Thailand, and Taiwan, among others) over the period 2000 - 2011. In the study it is depicted that the influence of foreign capital inflows on housing prices differed in terms of country, this was mainly justified by macroeconomic policies prevailing in the countries that tended to be different. Gholipour et al. (2014) assessed the link between foreign real estate investment, economic development, and housing prices in 21 OECD countries over the period 1995 – 2008 by using the panel cointegration technique. It was concluded that FREI did not influence housing prices in the short and long term.

Studying regional housing prices for 15 regions in India and using quarterly data over the period 2010 – 2013, Mallick & Mahalik (2015) established that fluctuations in housing prices were justified by fundamentals and foreign direct investments. Using a fixed effects model, they depicted that real foreign direct investment had a positive significant influence on housing prices in India. For the Singapore context, Chow & Xie (2016) used an autoregressive distributed lag method (ARDL) and quarterly time series data over the period 2000 – 2013 and found a short-term positive link between housing prices and FREI. It was observed that foreign inflows had a more significant influence on housing prices as compared to other domestic factors such as gross domestic product or the stock market.

A preliminary study on the influence of FREI on land prices in Mauritius was undertaken by Brooks et al. (2017) using a pooled panel regression approach with data over the period 2006 – 2013. They used the prices of the residential infrastructures sold to the foreigners and the land prices prevailing in the specific regions where the developments had taken place and concluded that the foreign investments had led to regional land price increases situated between 4% – 22%. This study was more focused on the regional influences of FREI on land prices and studied the relationship between the variables over a relatively short time span, without integrating the influence of other control variables on land prices. Wortman et al. (2016) also studied how foreign investment generating residential tourism affected the inhabitants of one particular region in Mauritius, namely Tamarin. Through an interview-based approach, it was concluded that residential land prices had increased in the region.

Studying the determinants of housing prices in Malaysia with quarterly data spanning from 2005 – 2013, Wong et al. (2019) used a fixed effects model (FEM) and a pooled mean group (PMG) approach to confirm that foreign inflow was significant in explaining the rising housing prices. More recently, using data over the period 1972 – 2018, Ahmed et al. (2021) studied if foreign capital inflow affected housing prices in Pakistan. A significantly positive relationship was found between housing prices and foreign capital inflow. They reported that the foreign inflows in the housing market led to job creation, increased the supply of capital, and promoted construction and development in the domestic context.

Although most studies on the nexus between foreign investment and real estate prices have focused on developing countries, a few studies have been conducted in developed countries that have benefitted from substantial levels of FREI. Studying the housing market in UK and Wales and using data over the period 1999 – 2014 with an instrumental variables approach, Sa (2016) found that foreign investment led to price increases in the housing market. It was also illustrated that in some regions the relative price increases had been higher and as per the study these represented the regions having obtained higher levels of foreign investment. The study depicted a positive significant link between FREI and housing prices, with an increase of 1% point volume in FREI leading to an increase of 2.1% in housing prices.

Ye et al. (2017) studied how housing prices in Canada were affected by foreign investments from China over the period 2009 – 2016 by using cointegration analysis and an error correction model (ECM). Two specific regions in Canada, namely Toronto and Vancouver were studied with both regions being affected to different extents by foreign investments, mainly in terms of the long and short-term effects. The study illustrated a causal relationship between housing prices in China and Canada, with the causality mainly from China to Canada. Studying housing prices in Australian states, Gholipour et al. (2019) used annual data from 1990 – 2013 and a panel cointegration approach. They differentiated the foreign residential real estate investments into two main types, namely existing residential real estate and new real estate developments and they individually assessed how each investment type affected housing prices. In the long run, no significant link was found between housing prices and foreign investment in existing residential real estate. Whereas foreign investment in new real estate developments had a significant negative effect on housing prices. From the short-run results, the two types of foreign investments did not have a significant influence on housing prices. In the study, a panel vector error correction model was used to establish the direction of causality between the variables, and in the long run, housing prices did not affect FREI.

Studying how foreign demand has affected real estate in Spain, Alvarez et al. (2020), found a significant positive influence on housing prices. This result was mainly justified by higher demand for properties situated on the islands and the Mediterranean coast, where higher housing price increases were noted. The demand for housing along the coastline and on the islands normally came from higher-income earners, willing to pay higher prices and thus causing more significant housing price increases in these regions.

The availability of data records on foreign real estate investment is quite limited, explaining the use of different measures as a proxy and which might not be accurate under all circumstances. The present study uses the annual figures of FREI over the past twenty years and is more accurate for the residential sector, given that most of the FREI is undertaken in that sector in Mauritius. It should prove to be a better measure when gauging the relationship between foreign investment and residential land prices. Most studies (Ahmed et al., 2021; Chow & Xie, 2016; Gholipour, 2013; Gholipour et al., 2014; Mallick & Mahalik, 2015; Tillmann, 2013 and Wong et al., 2019, among others) undertaken over the past decade have focused on how FREI affects housing prices and this study will be an addition to the scant literature on land prices.

Foreign real estate investment has been important in island economies over the past decades and only a few studies undertaken on this topic (Álvarez et al., 2020; Brooks et al., 2017; Mihaljek, 2005; Rose & La Croix, 1989; Wortman et al., 2016). From the island state’s perspective, only a few conceptual or survey-based studies were undertaken in the following contexts, Croatia (islands) and Mauritius to study the link between FREI and real estate prices. This study is considered as being more comprehensive in terms of the factors and the time span used for explaining land prices, as well as the measure used for FREI.

3. Methodology

Structural Time Series Model

In its simplest form, the structural time series model specified by Harvey (1990) can be used to express land prices as follows:

LPt=μt+εt

where represents the trend component and is the random component, with εt NID (0,

The trend represents the long-term movement in land prices and it can further be decomposed as follows:

μt=μt−1+νt−1+ηt

νt=νt−1+ξt

Equation 1 is also known as a local linear trend model assumes that the trend is stochastic, such that the slope and level change over time. The disturbance terms are mutually independent and distributed as follows: ηt NID (0, and ξt NID (0, When the trend follows a random walk with drift and if then it contains a deterministic linear trend. Whilst and results in a smooth trend model.

The model specified in equation 1 is estimated by using the maximum likelihood estimation technique and the Kalman filtering for updating the state vector. The specificity of the aforementioned estimation technique is that a time-varying parameter framework is applied, where the parameters vary over time.

Structural Time Series Model (STM) and Explanatory Variables

Equilibrium Land Price

The explanatory variables used for land prices would be demand and supply side factors. The equilibrium market price of land is established through the interaction of land demand and supply.

The total land demand emanated from the demand made by locals (domestic demand), the demand made by foreigners (foreign demand), latent variables, and the function for the quantity of land in demand at time t are given as follows:

Dt=f(LPt,It,Unempt,Popt,IRt,LVt,FREIt)

Where Dt is land demand, LPt is land price, It is income, Unempt is the level of unemployment, Popt is the population size, IRt is the interest rate, LVt is latent variables and FREIt is the level of foreign real estate investment. All the aforementioned variables are specified at time t.

The function for the quantity of land in supply at time t is as follows:

St=f(LPt,RBPt,CCt,LVt)

Where St is land supply, LPt is land price, RBPt is residential building permits, CCt is the construction costs, LVt is latent variables. All the aforementioned variables are specified at time t.

At equilibrium land demand should be equal to land supply and the equilibrium land price at time t is as follows:

LPt=f(It,Unempt,Popt,IRt,RBPt,CCtFREIt,LVt)

Foreign Land Demand

Apart from the trend, other unobserved components, such as cycles and seasonal components can also be included in the structural models. From Harvey & Shephard (1993) a univariate structural time series model can be extended with the inclusion of explanatory variables, which appear alongside the unobserved components in the model. The specificity of the structural time series model when including explanatory variables is that the link dependent – explanatory variables vary over time. The following model is used to ascertain if FREI has a significant influence on aggregate land prices or if other unobserved variables are contributing to land price fluctuations.

LPt= μt+ ϕt+φtFREIt+ εt

The unobserved components in the model are denoted as μt (trend component), ϕt (cycle component) and εt (irregular component). The coefficient φt measures the influence of FREI on residential land prices. The estimated coefficient φt is time-varying and it measures if the link land price – explanatory variable changes over the study period.

Domestic and Foreign Land Demand

Similar to Hannonen (2005) studying land price determinants, the structural time series model used is an extended version of an ordinary least squares method and it incorporates three stochastic components, namely a trend, cycles, and an error term. The equilibrium pricing model includes both domestic demand/supply and foreign demand factors is used (similar to Rose & La Croix, 1989). To distinguish if it is domestic land demand or foreign land demand or if supply-side factors are leading to fluctuations in residential land prices, the following structural time series model is used.

RLPIt=μt+ϕt+φ1tFREIt +φ2tRPCEt+φ3tPOPt+φ4tRIRt +φ5tUNEMPt+φ6tRBPt+φ7tRCCIt+εt

represents the time-varying coefficient associated with each independent variable. RLPI represents the real land price index used as a measure of land price; RPCE is the real per capita earning and used as a measure of income; POP is the population size; RIR is the real interest rate; UNEMP is the level of unemployment; RBP is residential building permits; RCCI is the real construction cost index and FREI is foreign real estate investments in the residential sector.

To find which model specification is most appropriate, namely between a log-log or a log-linear or a linear specification the model selection criteria namely the Akaike Information Criteria (AIC), Schwartz’s Bayesian information criterion (SC), and the Hannan-Quinn information criterion (HQ) are used. The model specification with the lowest values for AIC, SC, and HQ is chosen and for all the regressions it is found that these values are minimized for the log-log specification. An advantage of using a log-log specification is in terms of the interpretation of the coefficients given as elasticities, where the dependent variable will vary by a given percentage amount, following a one percent change in the explanatory variable.

Dependent and Independent Variables

Land Price (RLPI)

For the analysis of the national land price, the yearly average residential land price is estimated by using the land prices prevailing in thirty-two regions in Mauritius over the period 2000 – 2019. The national average land prices are then converted into their real values and a land price index is estimated using the real values.

Foreign Real Estate Investment (FREI)

FREI measures the level of foreign investment in the real estate sector. Three schemes, namely the integrated resort scheme (IRS), real estate scheme (RES), and the property development scheme (PDS) constitute the main sources of foreign investment in Mauritius over the past decades and all three schemes are in the residential real estate sector. As the demand for residential schemes increases, residential land demand would be increasing and this should be increasing land prices. Studying the influence of FREI on housing prices in 21 emerging countries, Gholipour (2013) found a positive significant link between the variables. In Sa (2016) foreign investment positively influenced housing prices. Undertaking a similar study in OECD countries Gholipour et al. (2014) found that FREI does not affect housing prices.

Income (RPCE)

As a proxy for income, the real per capita earning is used and it normally measures the purchasing power of individuals. An increase in income in the local context should normally lead to an increase in domestic demand. Using a similar measure for income Rose & Lacroix (1989) depicted that domestic income has a positive significant effect on local land prices. Ahmed et al. (2021) depicted a significant positive link between domestic income and housing prices. Mallick & Mahalik (2015) who included real income as a determinant of housing prices found no significant link between the variables.

Population (POP)

The aggregate value for the Mauritian population aged between 15 – 65 years is used. An increase in the local population should entail an increase in domestic residential land demand and prices. From Rose & Lacroix (1989) it was found that the domestic population had a positive and significant influence on land prices. A positive significant relationship between housing prices and the population is observed by Ahmed et al. (2021). According to Mallick & Mahalik (2015), the main variable affecting housing demand and subsequently housing prices should be population size.

Real Interest Rate (RIR)

The level of interest rate prevailing in the domestic market should be affecting the local demand for residential land. The real cost of funds for a borrower, that is taking into consideration inflation, is measured by using the real interest rate. A low mortgage interest rate should be encouraging individuals to borrow for land purchases, hence land demand and consequently land prices should be increasing. A negative significant link was observed between interest rates and housing prices by Adams & Fuss (2010). Gholipour (2013) concluded that interest rate does not have a significant influence on housing prices in emerging economies.

Unemployment (UNEMP)

The unemployment level is used to measure land demand. As more individuals are employed (decrease in unemployment) in the local context, they would be increasing their land demand and this should be increasing land prices. In Sa (2016) it is found that the local unemployment rate has a negative significant influence on housing prices.

Residential Building Permits (RBP) and Real Construction Cost Index (RCCI)

The explanatory variables residential building permits and real construction cost index are used as supply-side factors in the domestic market. In some past studies namely Rose & Lacroix (1989) and Sa (2016), it has been justified that foreign investments have a higher positive influence on land prices due to limitations in terms of domestic supply. Hence the importance of including supply-side factors as land price determinants.

Data

The data for the study has been collected every year over the period 2000 – 2019. The Mauritian real estate market is accessible to foreigners since the year 2000. The two decades of data available will allow discerning if there has been any particular trend, cycle, seasonal or irregular pattern in land price evolution that could be explained by FREI (Jebb et al., 2015). The main variable studied is land prices and an average land price index for Mauritius has been estimated. Land price data collected from thirty-two regions has been retrieved from valuation officers and used for calculating the average land price index. Data relating to population size, unemployment level, residential building permits, and construction cost index is obtained from the website of Statistics Mauritius while the data for income (earnings) and the real interest rate was collected from the website of the World Bank. The foreign real estate investment (FREI) figures have been collected from the Bank of Mauritius.

A structural time series model (STM) is used on the time series data, to find the link between FREI and residential land prices. Using STM, it is studied if residential land price increases are due to an increase in domestic land demand or due to an increase in foreign real estate demand or if supply-side factors have been affecting land prices or if other unobserved components are influencing land prices.

4. Data Analysis

Analysis

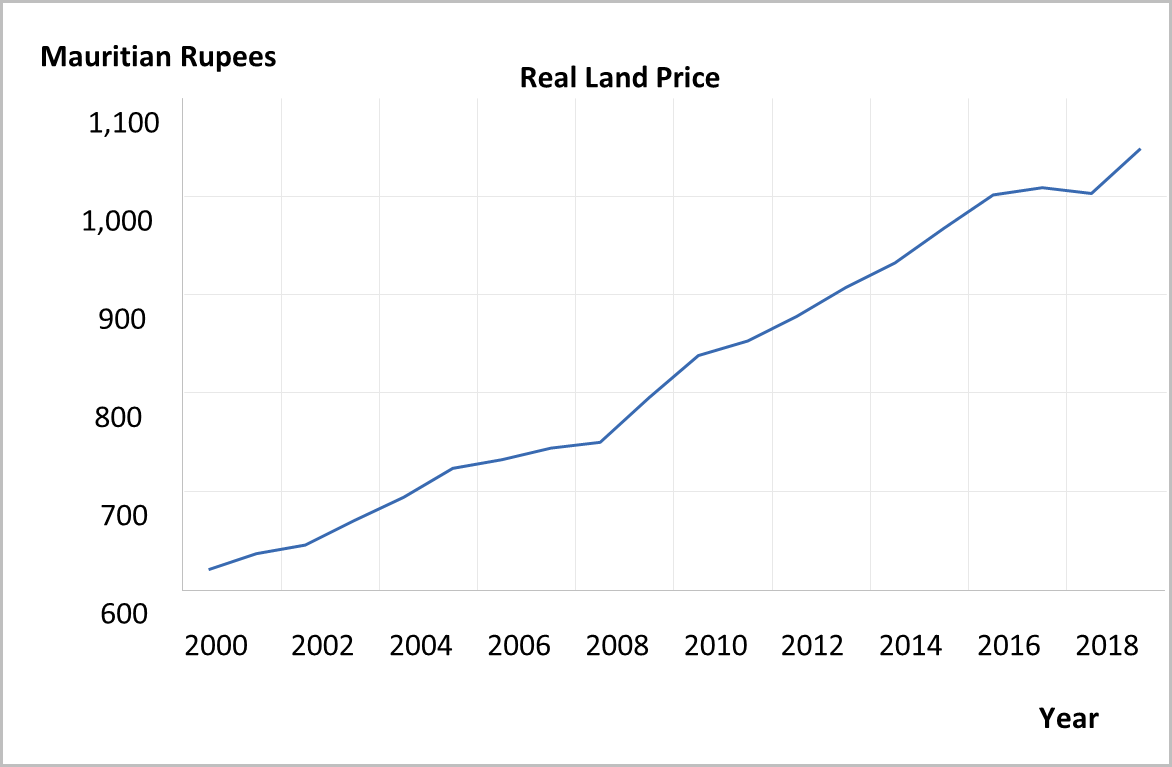

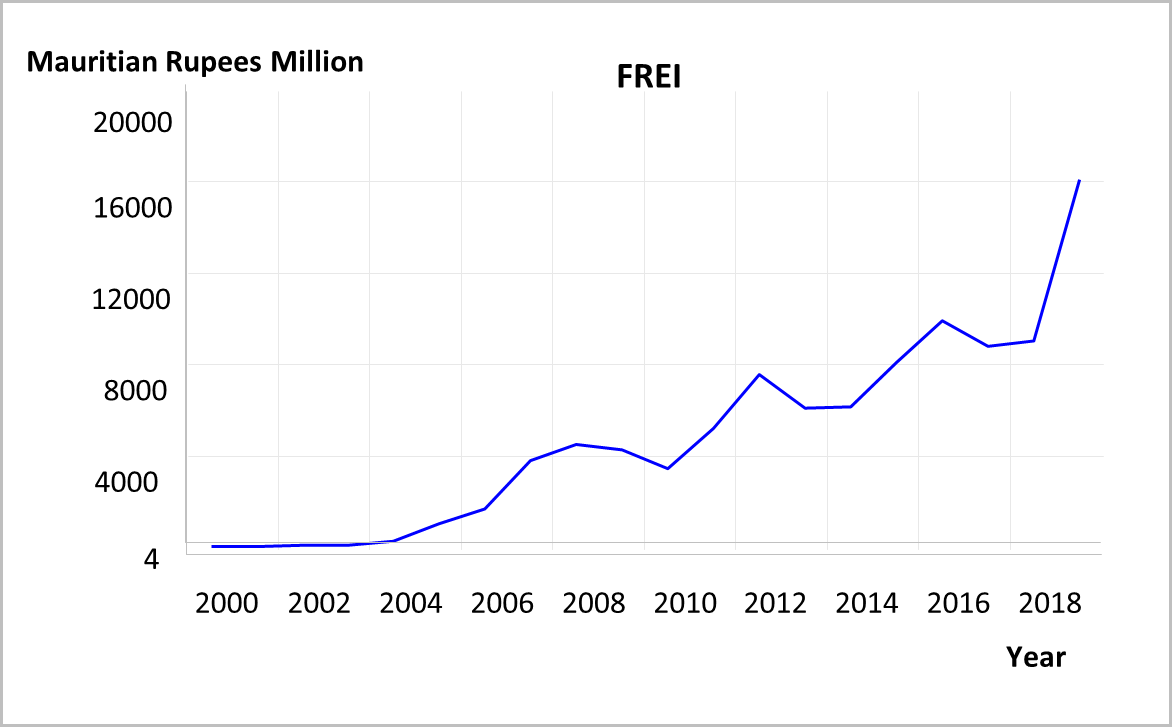

A comparison of the two main variables being studied illustrates that the changes in land prices have been more gradual as compared to changes in FREI, with higher dispersion in the FREI figures. From Figures 1 and 2, it is observed that real land prices and FREI have been increasing over the past twenty years.

Structural time series model

The STM is used to estimate if FREI affects national residential land prices. The regression results are given in Table 2. It is depicted that FREI does not influence residential land prices on a national basis. From Chan (2007), real estate prices should not be affected by FREI as foreign land demand represents a small proportion of the total demand in the real estate market. Gholipour et al. (2014), studying 21 OECD countries, found that there is no significant link between FREI and housing prices. In Australia, Gholipour et al. (2019) also found an absence of a significant relationship between FREI and housing prices. The results show that both the trend level and slope are significant in explaining the land price changes. Illustrating that latent variables have been causing land prices to increase. For example, grants provided to first-time homebuyers or other tax relief facilities on mortgage loans (Algieri, 2013). The medium-term cycles are also causing significant variations in land prices. The R2 value of 0.63 also suggests that there are factors, other than foreign land demand which are explaining the residential land prices in Mauritius.

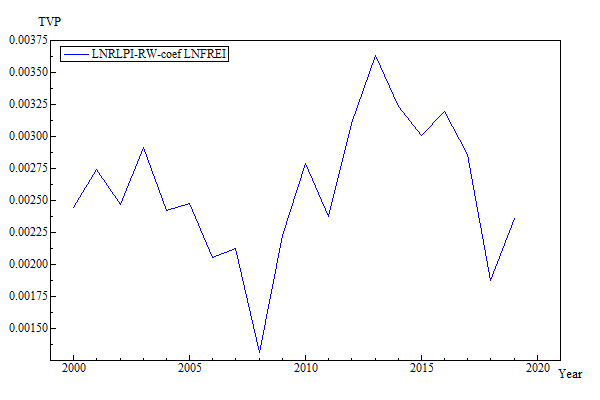

Although FREI is not significant in explaining real land prices, the time-varying coefficient has been fluctuating over the period 2000 – 2019. It is observed that the lowest coefficient occurs over the financial crisis period and post the crisis period the coefficient measuring the magnitude of the relationship between land prices and FREI has been increasing. According to Tillmann (2013) and Wong et al. (2019), the financial crisis has pushed real estate investments in Asian/African markets.

_measuring_the_relationship_between_real_land_price_and_frei_o.png)

To obtain a better insight into the factors causing land price fluctuations over the study period, local demand for residential land is included in the model, as well as two supply-side factors. In the Mauritian context, it is important to include the demand-side factors, mainly considering that over the past decades, the population size has been increasing, as well as income, whilst both interest rate and unemployment have been fluctuating. Factors such as construction costs and the number of residential building permits approved are included, as these have been varying and influencing the supply and subsequently price of land. The unobserved components and the foreign land demand factor are also included in the model. The results obtained from the extended version of the structural time series model, containing explanatory variables are given in Table 3.

The results obtained when including other explanatory control variables (domestic factors affecting land demand/supply) also lead to the conclusion that FREI does not affect land prices and that foreign land demand is insignificant in explaining domestic land prices. The explanatory variables included in the model explain a larger proportion of the variation in land prices from the R2 of 0.88. Among the local demand side factors, income and population are positively related and have a significant effect on land prices. Past studies, for example, Jud and Winkler (2002), have found population and income as being important determinants of real estate prices. It is noted that unemployment has a small positive influence on land prices, although most past studies (Gan et al., 2018; Liu et al., 2016) have concluded an inverse link between the two variables. Among the supply-side factors, real construction cost has a positive significant effect on land prices and Lerbs (2014) also detected a positive relationship between the two variables. This might suggest that the rising construction costs lead to a decrease in real estate supply (inelastic supply), which could entail an increase in housing/land prices.

The unobserved components in the model, namely the level, slope, and cycle (1) are significant in justifying land price fluctuations. Land prices have a positive and increasing trend. According to Algieri (2013), the unobserved components represent the influence of latent variables on residential land prices, such as the tax relief on the mortgage interest rate, land supply restrictions and zoning regulations among others. The results obtained illustrate that in the Mauritian residential land market prices are mainly determined by domestic demand, supply and other regulations specific to the local residential market.

Discussion

This study suggests that in the residential land market, the main factors affecting the prices have been domestic land demand and supply. Whereas foreign land demand did not have a significant influence on residential land prices.

Real estate prices in some countries have undergone significant price increases, for example, China, Australia, Switzerland, and Canada, among others (Sa, 2016). These countries have set up particular policies with the aim of restricting real estate investment by foreigners. Such policies have mainly been implemented in developed contexts. Several studies on the link between FREI and real estate prices have found either no relationship or a weak relationship between the two variables (See Gholipour, 2013; Gholipour et al., 2014, 2019 and Wong et al., 2019). According to the aforementioned authors, emerging countries should continue promoting FREI given its weak or no influence on real estate prices and the various benefits it generates for the domestic country. Wong et al. (2019) advocated appropriate monitoring measures to be set up so as not to lead to affordability issues for the natives in the real estate market. Responsible authorities and other regulatory bodies in Mauritius should promote FREI given the important benefits that it generates for national development. For example, FREI has been leading to job creation and enhancing the living standard of Mauritians in the coastal regions of the island (Wortman et al., 2016). The island should benefit from the foreign investments that allow economic development, whilst at the same time managing the use of natural resources and the development of the coastal regions in Mauritius. In some countries, for example, Spain and Croatia, where coastlines and islands have been receiving important foreign investments, governments have adopted regulations to better manage the developments. With the aim of not completely modifying the landscape in the region, as well as preventing residents from feeling alienated in their own country.

Most of the FREI is concentrated around the coastline of Mauritius and represents the preferential regions for residential tourists. The properties sold to foreign investors are essentially luxurious apartments or villas, selling at relatively higher prices. Such properties should normally be influencing the prices of adjacent real estate. Nonetheless, the results obtained illustrate that this influence has not been at the national level, suggesting that FREI is not significantly influencing land prices in other urban or rural regions. However, close monitoring of land prices in different regions should be maintained to assess how FREI is affecting land prices over time. To ensure that Mauritian residents are not being outpriced from the real estate market due to foreign investors.

The main limitation remains the availability of data on foreign real estate investments over a longer time series and also on a regional basis. Other variable/s could have been included in the model as measure/s of foreign residential real estate demand, for example, the number of foreign inhabitants (residing in the long term, for example, residential tourists) in Mauritius over the study period. However, the unavailability of consistent data series over the study period remained a limiting factor.

5. Conclusion

This study was undertaken to understand the evolution of residential land prices on the island of Mauritius. The specificity of the Mauritian real estate market is that over the past two decades, there has been a surge in foreign real estate investments. More specifically this research attempted to establish if land price increases observed in the market over the past decades have been caused by domestic land demand, foreign land demand, or domestic land supply.

Using a structural time series model it is concluded that foreign land demand (as measured by FREI) does not influence land prices. To find whether domestic land demand and supply are determining factors in the formation of land prices, an extended version of the structural time series model containing control explanatory variables is used. The regression results obtained allow us to conclude that domestic demand side factors, such as income and population are significant in explaining land prices. Whilst on the supply side construction costs are found to significantly influence land prices. The unobserved components, namely the slope and cycles are also important in justifying land prices, thus suggesting that there are latent (non-measurable) variables such as land regulations (affecting land supply) or tax reliefs on mortgage interest rates or zoning regulations that determine land prices.